Will they or won’t they? Taxpayers have been anxiously waiting for Congress to make decisions about cutting tax rates for months. With no answer so far, on December 31, 2012, the so-called “Bush tax cuts” will expire. Those cuts were initially set to lapse in 2010 but were temporarily extended for two years due to legislation signed in December 2010. Now, the cuts are up for debate again and so far, there’s been no movement.

![Couple discussing taxes]()

Here are 11 tax changes looming in 2013 and what they mean for families:

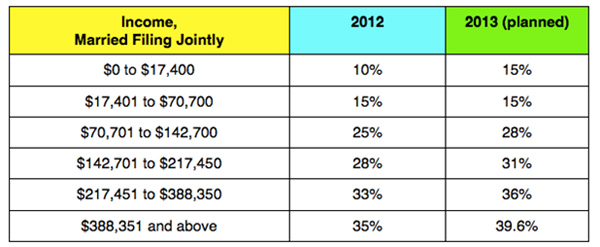

Income tax rates

Income tax rates are going up. For the last several years, tax rates have been relatively low, making it possible for a family of four to have a federal income tax bill of zero on nearly $60,000 of income. That will change in January as tax rates increase for nearly all brackets. Here’s how, for example, married taxpayers will be affected:

![Income tax rates]()

Alternative Minimum Tax

The Alternative Minimum Tax will affect nearly 30 million additional taxpayers. The exemption amount for the AMT is not indexed to inflation which means that Congress must “patch” the exemption each year to keep pace with inflation and other increases. The most recent exemption amounts are $74,450 for those taxpayers filed as married ; without a patch for 2012 or 2013, the AMT exemption amounts will be $45,000 for those taxpayers filing as married . Those lower exemption amounts mean more families are affected and may pay higher taxes; if you are subject to the AMT, you figure your tax rate two times and pay the higher amount.

Dividend rates

Dividend rates will be re-characterized. Currently, dividends are taxed as capital gains or ordinary income, depending on the nature of the dividend. In most cases, it’s more advantageous to be classed as capital gains. However, at the end of 2012, all dividends will be taxed as ordinary income; that includes dividends which are re-invested in DRIP .

Capital gains tax rates

Capital gains tax rates will increase. Capital gains tax is, at its most simple, the tax paid on the difference between the sales price of an asset and its cost. Capital gains rates are low at present, at just 15 percent for most taxpayers. In January, those rates will increase to 20 percent for assets not inside a tax-deferred account; remember that gains and losses inside a tax deferred account are not realized, fortunately, until you take the money out.

Unearned income and Medicare tax

Unearned income, generally income from sources other than wages , is currently exempt from Medicare tax. That’s changing in 2013 when a Medicare tax of 3.8 percent will be imposed on unearned income for high income taxpayers. Fortunately, while children subject to the kiddie tax are taxed at their parents’ rates for purposes of the Medicare tax, the normal rules for children’s income still apply which means that children are not subject to the tax just because their parents might be.

Medicare surtaxes

Medicare surtaxes will be imposed on high income taxpayers. Beginning in 2013, the Medicare tax imposed on high income taxpayers will be increased by 0.9 percent to 2.35 percent for wages over the income thresholds .

The payroll tax cut

The payroll tax cut will disappear. The payroll tax cut, which reduced payroll tax contributions on the employee side by 2 percent, was intended to last just one year but was extended into 2012. It expires at the end of the year and will not be in place for 2013. That means that all families with at least one working parent will see at least a 2 percent decrease in their take-home pay.

Limits on exemptions and deductions

Exemptions and deductions will be limited for high-income families. The general rule is that as income increases, personal exemptions and itemized deductions decrease. That hasn’t been the case for the last few years when families in all tax brackets could take advantage of personal exemptions and itemized deductions. In 2013, the original thresholds, indexed for inflation, will be reinstated. That means that families in the top brackets will not be able to claim all of their personal exemptions for dependents; itemized deductions will also be reduced. The result? It basically bumps the top tax rate up even higher for those in the top brackets.

Child tax credit

Credits for families with children will also be reduced. Credits are generally more desirable than deductions because they reduce tax due on a dollar for dollar basis . Under the current tax scheme, families could claim up to $1,000 per qualified child as a child tax credit. In 2013, that amount is halved to $500 which could boost tax bills by up to $500 per child.

Medical deductions

Medical deductions will be harder to claim in 2013. Medical expenses for taxpayers who itemize are currently deductible to the extent that they exceed 7.5 percent of adjusted gross income ; that threshold is sometimes referred to as the “floor.” Beginning in 2013, taxpayers who itemize can only deduct those medical expenses which exceed 10 percent of AGI . That means that fewer families will be able to claim medical expenses, making pre-tax plans more attractive.

Education tax breaks

Tax breaks for education will be reduced. The American Opportunity Tax Credit for education is a souped-up version of the Hope Credit. It allowed families a credit of up to $2,500 for certain educational expenses; when it expires, the credit will revert to the Hope Credit and will be limited to $1,800. It’s also going to be more difficult to put money aside for education: Coverdell Education Savings Account contribution limits will be dramatically reduced from $2,000 per year to a mere $500 per student.

With all of these changes in store, what should you do? There is no crystal ball. And absolutely no one knows what’s going to happen in 2013. The best advice is to plan for tax laws in place as of today — but stay educated and be flexible.

More on family finances

Talking to your kids about family finances

Tips for adding to your child's college fund

The financial strain of special needs

Pizza

Pizza Pajama party

Pajama party